For large commercial and industrial consumers, BESS in Rajasthan has become a regulatory and financial consideration rather than an optional backup system. The state mandates storage for oversized captive solar projects and offers a wheeling-charge waiver that reaches 100% for consumers who pair solar with the required BESS ratio. This article sets out how that combination of mandate and incentive translates into project-level costs and savings.

Buyer Profiles Revisited

The Same Three Consumers, Now With Storage

| Profile | Part 1 Constraint | What BESS Changes |

|---|---|---|

| Captive auto-components manufacturer | Paying wheeling charges on every wheeled unit — exempt from Cross-Subsidy Surcharge and Additional Surcharge as a captive structure, but with zero banking on surplus | Can take the wheeling and transmission line to zero for seven years by pairing the open-access contract with a BESS sized to the qualifying ratio |

| Rooftop textile manufacturer | Net-metered solar never touched the evening peak surcharge | Can now discharge stored midday solar directly into that evening window — avoiding the 10% surcharge, and staying outside the Parallel Operation Charge because the capacity remains behind the meter |

| Captive solar generator | Losing units to the banking ceiling every strong-generation month | Can capture that surplus directly in storage instead of relying on a DISCOM banking allowance that was not large enough to hold all of it |

As in Part 1, the worked numeric examples below — a 4,000 kVA medium industrial (MP/HT-3) consumer and a 1,000 kVA commercial (NDS/HT-2) consumer — are illustrative figures distinct from the three profiles above.

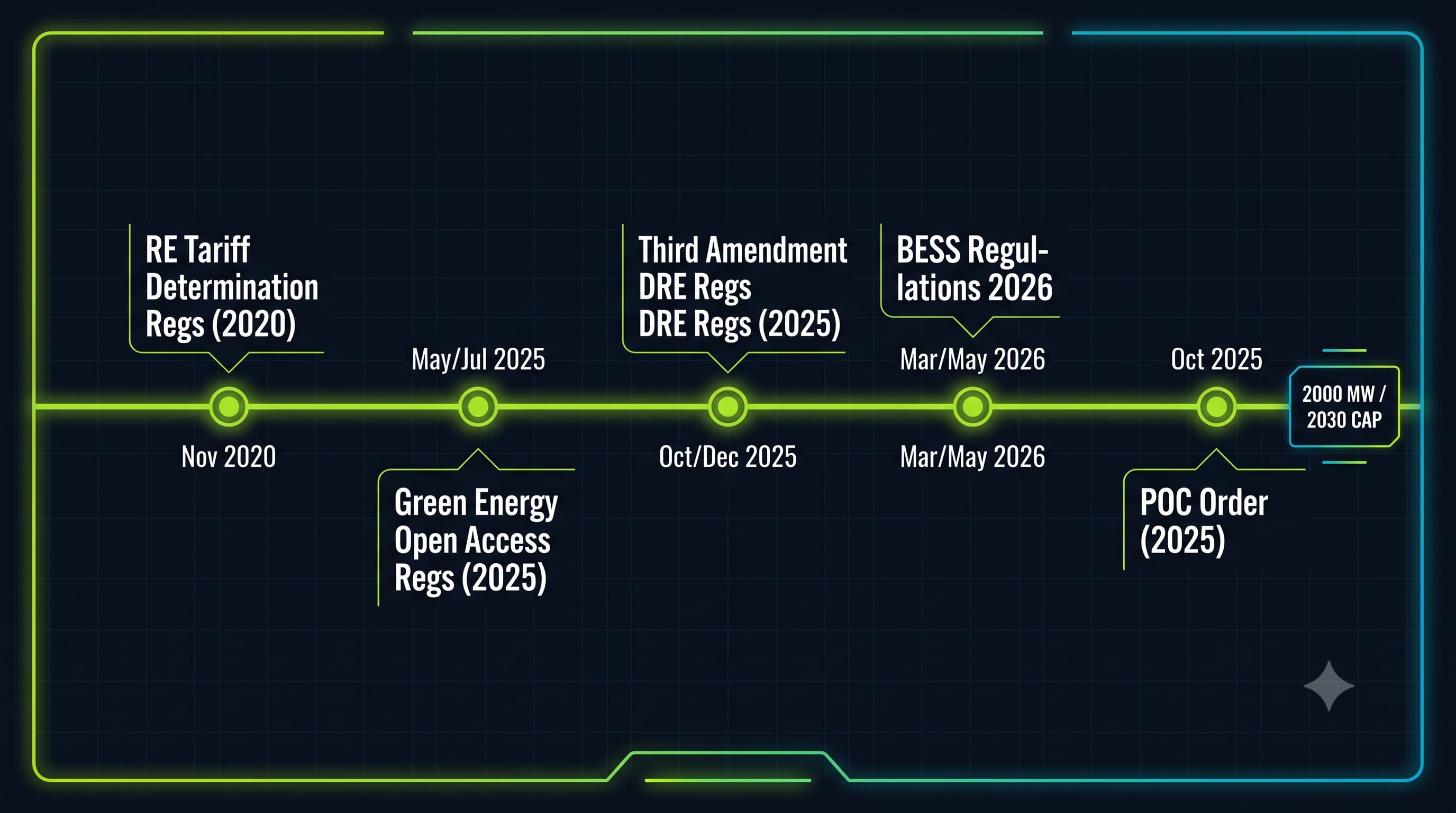

The RERC BESS Regulations 2026

Five Regulatory Instruments, One Framework

Rajasthan's BESS framework consists of five regulatory instruments issued between 2020 and 2026, summarized below with the applicable regulation for each.

| Instrument | Notified / Gazetted | Core Subject |

|---|---|---|

| RE Tariff Determination Regulations, 2020 (Reg 138) | Nov 2020 / Dec 2020 | Generation tariffs, original 100% captive cap, superseded 75% waiver |

| Green Energy Open Access Regulations, 2025 (Reg 158) | May 2025 / Jul 2025 | 200% captive rule, 20% BESS mandate, banking, graduated wheeling waiver |

| Third Amendment to Grid Interactive DRE Regulations (Reg 159) | Oct 2025 / Dec 2025 | Net-metering wheeling relief, deemed feasibility ≤10kW |

| BESS Regulations, 2026 (Reg 164) | Mar 2026 / May 2026 | Dedicated storage framework, BTM registration, RPO retention |

| POC Order (Petition 2239/2024) | Oct 2025 | ₹11.90/kVA/month cost on renewable captive plants |

RPO Status and Renewable Energy Retention on Discharge

Under the RERC BESS Regulations 2026 (Regulation 9.4), solar-charged BESS energy keeps its renewable character on discharge, so RPO-obligated entities don't lose RPO/RCO credit by time-shifting through a battery. Two things worth being precise about, since earlier coverage has overstated both:

- Double-taxation avoidance is a stated principle, not yet a locked guarantee. The Regulations direct the Commission to follow this principle when it sets the actual settlement mechanism (Reg 164, §9.2(c)) — the mechanism itself hasn't been finalized.

- The incentivized tariff for non-solar-peak-hour injection exists in principle (Reg 9.2) but the rate is not yet notified, pending a separate Commission order. Worth watching, not worth budgeting around yet.

Cracking the 200% Captive Rule

Double the Ceiling, With a Storage String Attached

Under the RE Tariff Determination Regulations, 2020 (Reg 138), captive renewable capacity — including behind-the-meter — was capped at 100% of contract demand. Under the Green Energy Open Access Regulations, 2025 (Reg 158), that ceiling doubled.

| 2020 Baseline (Reg 138) | 2025 Update (GEOA Reg 5) | |

|---|---|---|

| Max captive RE capacity | 100% of contract demand | 200% of contract demand |

| Storage requirement on the oversized portion | None specified | 20% of energy from the >100% slice |

| Banking charge (≤100% CD tier) | 10% | 8% |

Capacity between 100–200% of contract demand must carry a BESS sized to store at least 20% of the energy generated by that incremental slice. This is not optional engineering headroom — it is a compliance requirement built into the sizing rule itself. (A separate, broader mandate applies alongside this one: any new non-hydro RE project above 5 MW on the STU network must install at least 2 hours of storage for 5% of RE capacity — a related but distinct trigger.)

Captive Solar Banking Ceiling and BESS Sizing Under the 200% Rule

Part 1's illustrative captive example showed a 4,000 kVA MP/HT-3 factory with a 3,000 kW captive rooftop system injecting 1,20,000 units of surplus in a strong-generation month against a banking ceiling of 90,000 units, leaving 30,000 units unbanked. Left unaddressed, Part 1's pecking order shows those units are worth anywhere from ₹0 (curtailed) to roughly ₹75,000 (exported at the generic solar rate of ₹2.50/unit) — a wide range, and not a good one.

A correctly sized BESS closes this gap, which is also why the 20% storage mandate on the 100–200% CD tier is not simply a compliance box to tick. If this factory were oversizing under the 200% rule, the mandated BESS would be sized against that same surplus: instead of injecting 1,20,000 units and relying on the banking ceiling to absorb enough of it, the battery captures the surplus directly and holds it for the factory's own later use, independent of the DISCOM ceiling. The full arbitrage math on these 30,000 units — including what changes if the capacity is also open-access wheeled — is worked through in the ToD Arbitrage section below.

Securing the 100% Wheeling Waiver

The Most Significant Financial Incentive in the Current Framework

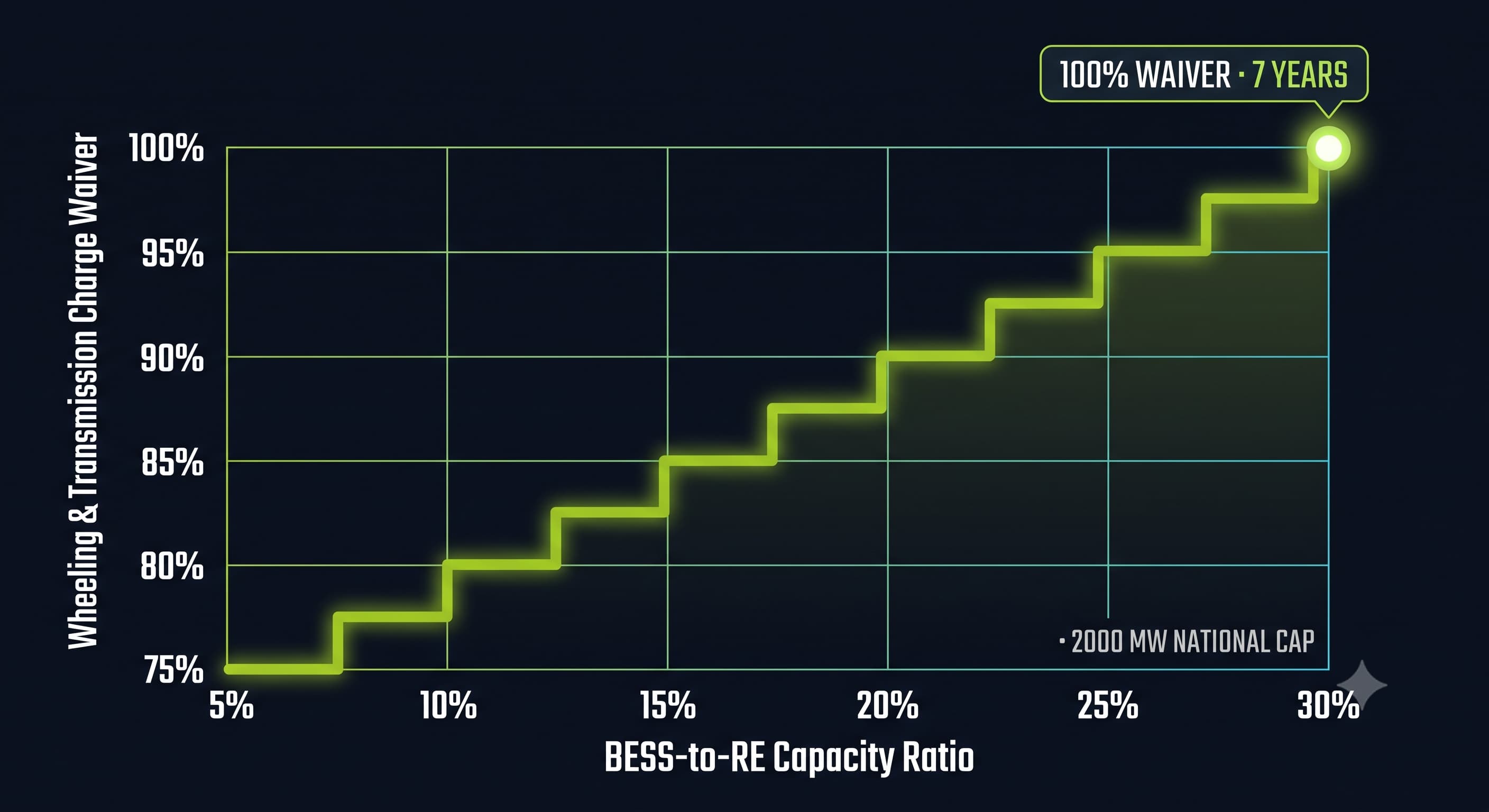

Under the Green Energy Open Access Regulations, 2025 (Regulation 11.3): for every incremental 1% of BESS capacity relative to RE capacity, from 5% to 30%, the exemption on transmission and wheeling charges climbs 1% — starting at a 75% waiver at the 5% threshold and reaching a full 100% waiver at 30% BESS-to-RE capacity.

Under the same regulation (Regulation 11.3, provisos (i)–(iii)), three variants apply — easy to conflate, worth keeping separate:

| Variant | Waiver | Duration | BESS-to-RE Threshold |

|---|---|---|---|

| RE-integrated storage | Graduated 75% → 100% | 7 years | 5% to 30%, scaling |

| Standalone BESS (peak / non-solar-hour supply) | Flat 100% | 7 years | Not ratio-based |

| BESS at 11kV/33kV grid substation | Flat 100% | No stated time cap | Not ratio-based |

ℹ Source: GEOA Regulations, 2025, Regulation 11.3.

The capacity cap is a firm constraint on the scheme: this is Rajasthan's second, more generous iteration of the waiver — the 2020 baseline offered a flat 75%, capped at 500 MW total (25 MW per plant), and that window closed 31 March 2023. Regulatory momentum has moved toward more generosity, not less, but the current window remains capacity-limited.

Wheeling Waiver Savings: Open-Access Illustrative Calculation

Illustrative figures only. Recall Part 1's open-access wheeling table: ₹0.62/kWh at 11kV. Applying this to the same 4,000 kVA MP/HT-3 factory used throughout this series — suppose 4,00,000 of its 5,00,000 units/month are sourced via captive open-access solar at 11kV:

| Line Item | Calculation | Amount |

|---|---|---|

| Monthly wheeling charge | 4,00,000 units × ₹0.62/kWh | ₹2,48,000 |

| Annualized | ₹2,48,000 × 12 | ₹29,76,000 |

| Over the 7-year waiver term | ₹29,76,000 × 7 | ≈ ₹2,08,32,000 |

Pairing that open-access contract with a BESS sized to the 30% BESS-to-RE threshold takes that entire line to zero for seven years. One important precision point: the waiver reaches wheeling and transmission charges only — and per Part 1, Cross-Subsidy Surcharge and Additional Surcharge don't apply to this factory in the first place, since it qualifies as captive generation. For this buyer, wheeling genuinely is the entire open-access-specific cost stack — which is exactly why eliminating it is worth over ₹2 crore across the waiver term.

Because this capacity is wheeled rather than co-located behind the meter, it also sits outside the Parallel Operation Charge covered later in this article — a structural difference from the captive and rooftop profiles above.

PWRNXT sizes your BESS to the 30% BESS-to-RE threshold on a zero-capex operating lease — so the wheeling waiver, the ToD arbitrage, and the banking-ceiling capture all stack on top of one investment you never had to make yourself.

Free · 5 working days · No capex commitment

ToD Arbitrage: Monetizing Storage

Two Value Streams, Modeled Separately

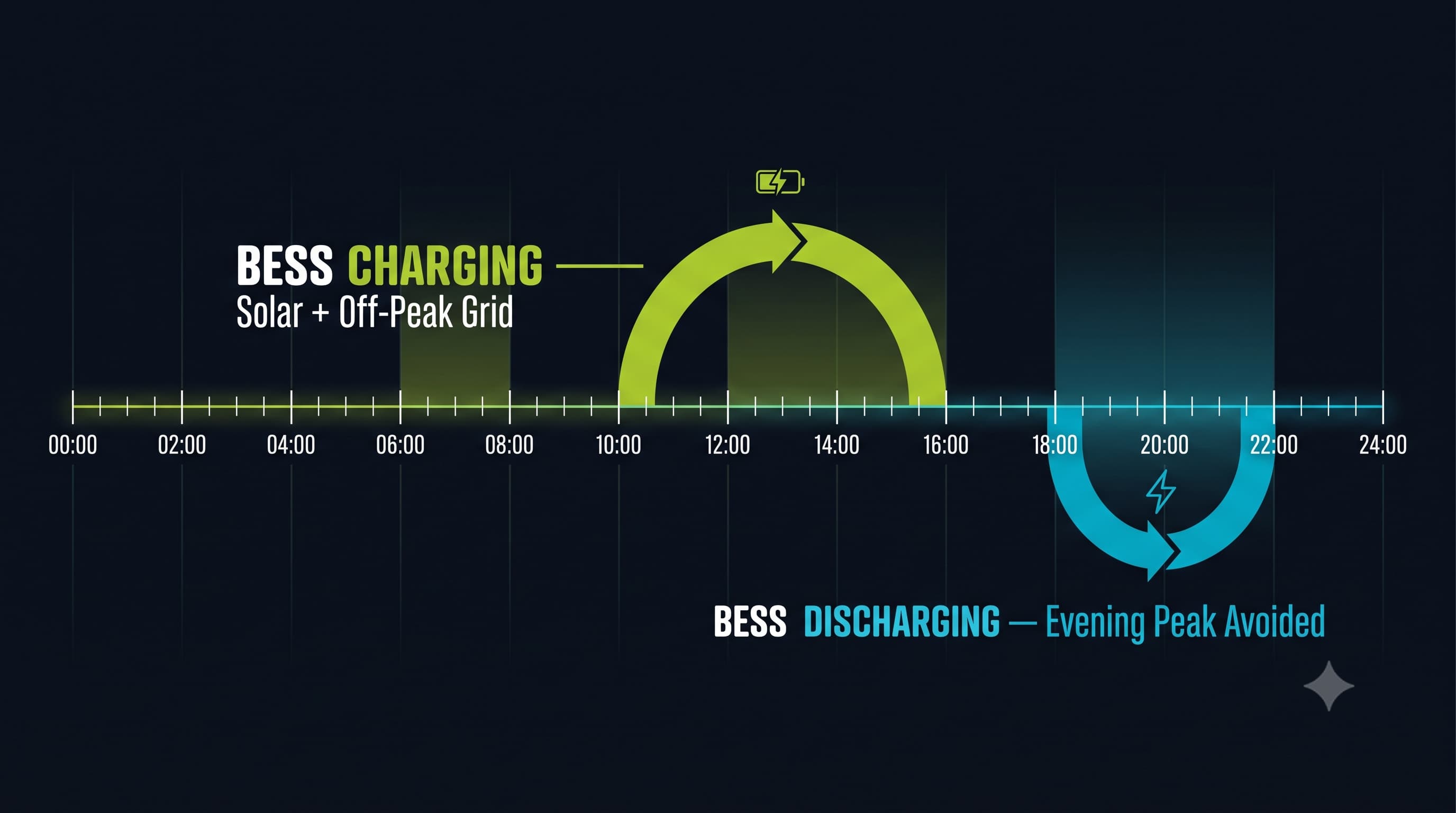

As set out in Part 1, solar generation cannot occur during Rajasthan's 6 pm–10 pm evening peak window. By the time the 10% surcharge applies, the sun has set, and no amount of solar capacity, on its own, offsets a consumer's most expensive hour of grid draw. Storage changes that. A BESS charged during the day — from onsite solar generation, or from the grid during the 12 pm–4 pm off-peak rebate window — and discharged during the evening peak captures value a solar-only installation cannot reach.

ToD arbitrage comprises two distinct value streams, which should be modeled separately rather than combined into a single figure:

- Grid arbitrage: charge from the grid at the 10% off-peak rebate rate, discharge to avoid the 10% evening-peak surcharge rate. The value captured is the spread between the two rates, minus round-trip efficiency losses.

- Solar self-consumption shift: charge from onsite solar that would otherwise be exported or banked, discharge during the evening peak instead. The value captured is the full evening-peak rate avoided, since the solar itself carries no marginal grid-purchase cost.

Continuing the Examples: ToD Arbitrage Value Calculation

MP/HT-3, 4,000 kVA industrial — grid arbitrage, illustrative:

| Rate | |

|---|---|

| Off-peak charging rate | ₹5.85/unit |

| Evening-peak avoided rate | ₹7.15/unit |

| Spread captured per unit shifted | ₹1.30/unit |

MP/HT-3, 4,000 kVA industrial — maximizing the arbitrage on unbanked surplus:

Part 1's pecking order for solar surplus ranked five options from most to least valuable, and named storage as the option this series' first article couldn't resolve on its own. Here's that resolution, applied to the same 30,000 units that fell outside this factory's banking ceiling in a strong-generation month.

The value of routing those units through storage instead depends on what would otherwise have happened to them — Part 1 gave two realistic baselines:

| Baseline (without BESS) | Value Without BESS | Value With BESS (evening peak, ₹7.15/unit) | Wheeling Charge Waived* | Total Value Unlocked |

|---|---|---|---|---|

| Curtailed / unrecovered | ₹0 | ₹2,14,500 | + ₹18,600 | ₹2,33,100 |

| Exported at generic solar tariff (₹2.50/unit) | ₹75,000 | ₹2,14,500 | + ₹18,600 | ₹1,58,100 (net gain) |

ℹ *Rooftop captive solar like this factory's doesn't incur wheeling charges in the first place — but many PWRNXT clients run offsite, ground-mounted captive or group captive plants that are wheeled to the facility. For that structure, the same BESS sized to capture the arbitrage above also clears the 30% BESS-to-RE threshold for the 100% wheeling waiver, adding ₹18,600/month (30,000 units × ₹0.62/kWh) on top. The two benefits stack because they come from the same BESS investment, not two separate ones — which is the core argument for sizing storage against the full regulatory picture rather than any single incentive.

Either way the baseline is framed, the pattern holds: storage recovers multiples of what curtailment or generic-tariff export would, and the wheeling waiver — where the capacity is wheeled — adds a further layer on top of that, not instead of it.

NDS/HT-2, 1,000 kVA commercial — resolving Part 1's opportunity cost directly:

Part 1 showed this Group Net Metering commercial complex settling 40,000 units of surplus for ₹3,14,500 (netted against its cheapest consumption first, per the lowest-tariff-slot-first settlement rule) against a theoretical ₹3,74,000 if that surplus could instead offset evening-peak draw — a ₹59,500 opportunity cost with no mechanism to close it.

| Without Storage (Part 1) | With Storage | |

|---|---|---|

| How the 40,000 units get used | Exported, netted against cheapest slots first | Stored, discharged directly into evening peak |

| Value realized | ₹3,14,500 | ₹3,74,000 |

| Gap closed | ₹59,500/month |

This example shows a constraint identified in Part 1 being addressed directly through storage design: the ₹59,500 was not a fee; it was value the settlement mechanics did not allow the building to capture. Storage captures this value directly, without relying on the settlement mechanism. Rooftop net metering doesn't wheel, so there's no equivalent waiver to stack here — the entire gain is the arbitrage itself.

Parallel Operation Charges & DISCOM Integration

The Cost the Wheeling Waiver Doesn't Cover

POC Rates and Applicability

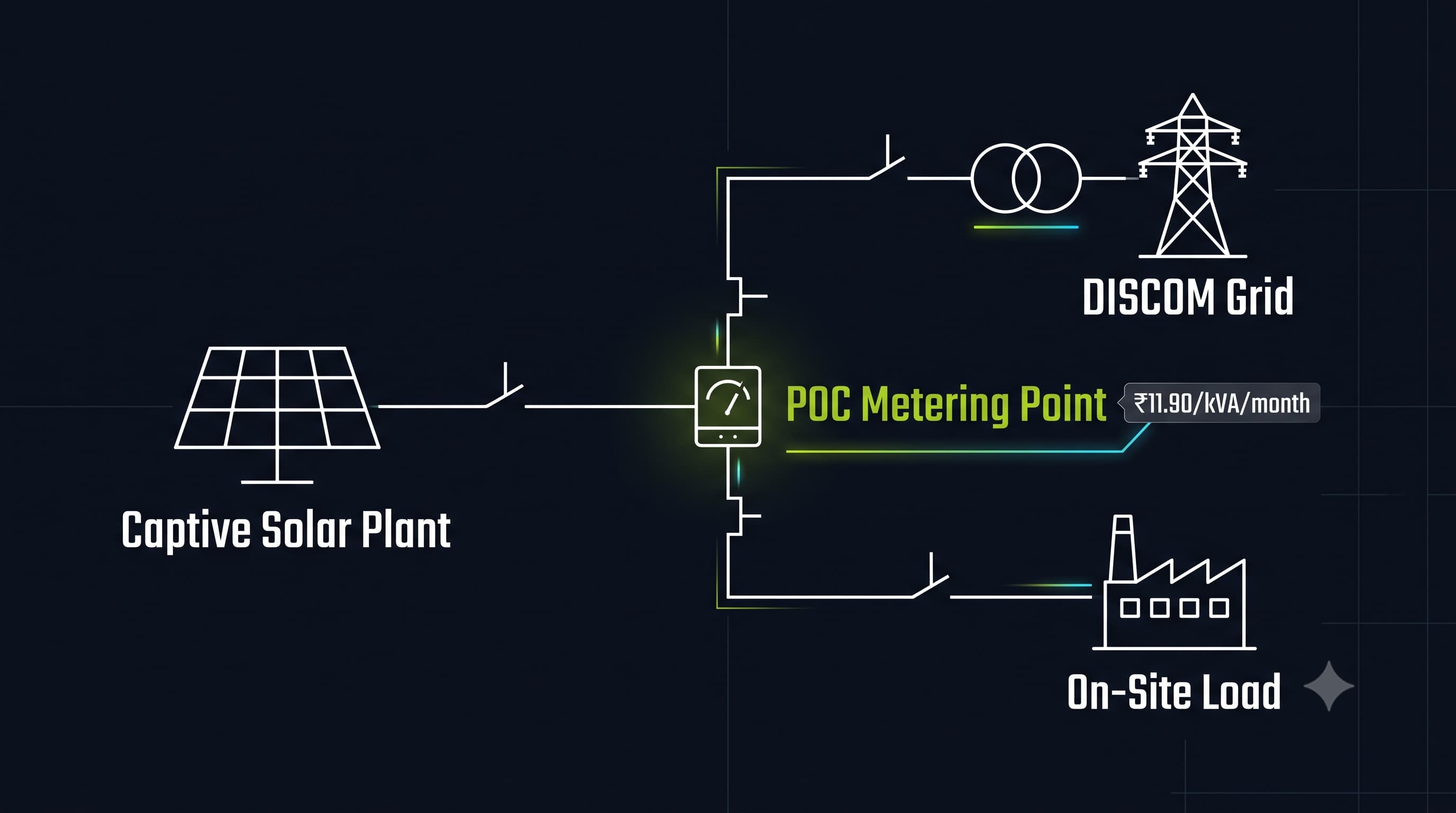

Under RERC's order on Petition 2239/2024, effective FY 2025–26, a co-located captive plant running in parallel with the grid now carries a charge for the grid-support benefits it receives — voltage support, harmonics absorption, fault-level support.

| CPP Type | Approved POC Rate |

|---|---|

| Conventional CPP | ₹27.237/kVA/month |

| Renewable CPP | ₹11.90/kVA/month |

| Hybrid CPP | Blended, pro-rata by capacity share |

| Rooftop solar (net/gross metering) | Exempt |

The exemption matters: this only applies to co-located, HT captive plants serving on-site load — not PPA capacity, not wheeled/offsite capacity (see the open-access example above, which sits outside POC entirely), and not rooftop-scale behind-the-meter projects under net or gross metering. A co-located HT renewable captive plant carries an ₹11.90/kVA/month cost on its net capacity that belongs in the same financial model as the wheeling savings.

BESS Registration and DISCOM Feasibility Requirements

Under the BESS Regulations 2026 (Regulation 15.1), behind-the-meter BESS registration runs through an online DISCOM portal, with no separate connection agreement required. Under the Third Amendment (Regulation 8.8), feasibility for domestic applications up to 10 kW specifically is deemed automatic — no technical study required.

This deemed-feasibility rule is domestic-only and capped at 10 kW; it does not extend to C&I-scale rooftop installations. A C&I project still goes through the standard technical feasibility process — it is the connection-agreement paperwork that has been removed, not the technical review itself.

Frequently Asked Questions

Common questions from Rajasthan C&I energy buyers about BESS regulations, wheeling waivers, and RPO retention.

PWRNXT Strategic Synthesis

The Complete Rajasthan BESS Business Case

The Maximum Value Stack: What BESS Actually Adds in Rajasthan

Every section in this article has quantified one lever in isolation. None of them run separately in an actual project — a single, correctly sized BESS is what unlocks all five at once, because they're triggered by the same underlying decision (pairing storage with captive or group captive solar) rather than five different investments.

| BESS Value Lever | Mechanism | Illustrative Value (4,000 kVA MP/HT-3) | Regulatory Basis |

|---|---|---|---|

| Wheeling & Transmission Waiver | 100% waiver at a 30% BESS-to-RE capacity ratio, for 7 years | ≈ ₹2.08 crore over 7 years, where the capacity is open-access wheeled | GEOA Regulation 11.3 |

| 200% Group Captive Headroom | Captive/group captive solar sized up to 200% of contract demand | Doubles addressable generation capacity — the precondition every other row depends on | GEOA Regulation 5 |

| ToD Evening-Peak Dispatch | Stored solar discharged at evening peak instead of drawn from the grid | Up to ₹7.15–9.35/unit avoided cost per unit shifted, by category | State tariff order, ToD schedule |

| Solar Surplus Capture Beyond the Banking Ceiling | Surplus otherwise curtailed or exported at ≈₹2.50/unit is instead stored and dispatched at evening peak | ₹1,58,100–2,33,100 in a single strong-generation month, illustrative | GEOA banking rules + ToD schedule |

| RPO/RCO Retention | Solar-charged BESS energy keeps its renewable character on discharge | Avoids RPO shortfall exposure on time-shifted generation | BESS Regulations 2026, Reg 9.4 |

The exact combination that applies — and the exact rupee figure — depends on a project's contract demand, load curve, sourcing structure, and generation profile. That's genuinely project-specific work, not something a generic table can finish for you. If you're evaluating a captive or group captive solar project in Rajasthan and want this stack modeled against your own numbers rather than an illustrative factory's, that's the conversation worth having with PWRNXT.

Model This Stack Against Your Own Numbers.

PWRNXT engineers a free BESS feasibility study for your Rajasthan facility — sized to your contract demand, load curve, and sourcing structure. Verified saving figure across all five value levers in 5 business days. Zero cost, zero obligation.